WHITE PAPER

Top 10 Things to Do

Before Refinancing or Sourcing New Loans

TABLE OF CONTENTS

- PREPARE FINANCIAL MODEL

- DETERMINE DEBT CAPACITY

- GATHER HISTORICAL FINANCIAL REPORTS

- PREPARE AN OVERVIEW OF THE BUSINESS

- LOAN PURPOSE

- CONSIDER DIFFERENT CREDIT FACILITIES

- OUTLINE BEST/WORST CASE SCENARIOS

- REVIEW EXISTING CREDIT AGREEMENTS

- SELECT COUNSEL

- DETERMINE YOUR TIMELINE

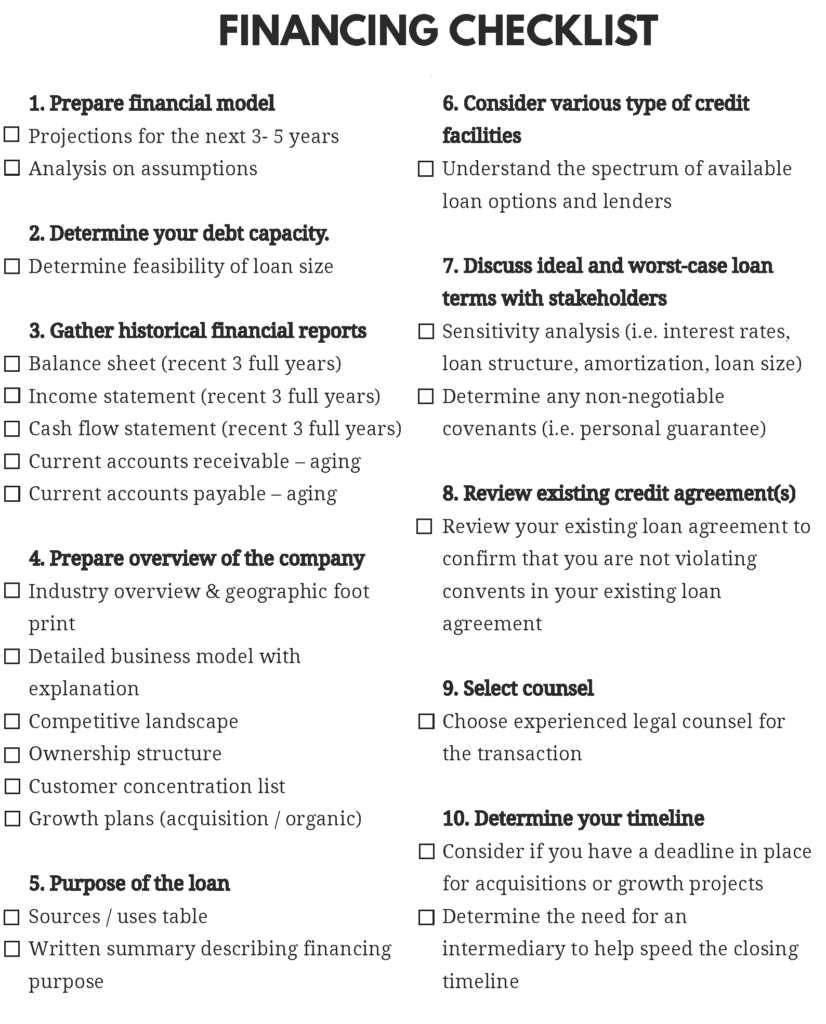

FINANCING CHECKLIST

Be ready to present the required materials before reaching out to any commercial lender. Preparation empowers you to negotiate the best terms for your company.

1. Prepare a Financial Model

Lenders expect three to five years of financial projections. Be ready to explain the reasoning behind your inputs and defend your assumptions. Clearly show how the requested financing will impact your future projections. With Cerebro Capital, you can access term sheet estimates to strengthen your scenario analysis and financial modeling.

2. Determine Debt Capacity

Analyzing your borrowing power in the current market helps set the right expectations. Use Cerebro’s Debt Capacity Calculator to confidentially estimate your company’s borrowing threshold and make informed decisions about the appropriate loan amount to seek.

3. Gather Historical Financial Reports

Compile comprehensive financial records:

- Balance sheets, income statements, and cash flows covering at least three years

- Corresponding tax returns and (when required) audited statements

- Up-to-date receivables and payables aging reports

- Additional items as applicable, such as equipment listings, recent real estate appraisals, inventory agings, and material contracts

Lenders will examine your financial history and the purpose of the loan in detail. Be prepared to answer specific questions about your industry, business operations, and intended use of funds.

4. Prepare an Overview of the Business

A strong business overview should address:

- Industry context and geographic footprint

- Detailed business model explanation

- Market and competitive landscape

- Ownership structure

- Customer concentration data

- Growth and expansion plans

A well-articulated overview reassures lenders about your management team’s clarity and your company’s positioning.

5. Loan Purpose

Develop a clear table outlining the sources and uses of funds for your planned initiative. Accompany this with a concise narrative explaining the need, rationale, and anticipated business value of the financing. Cerebro can assist in sharpening your loan request narrative to maximize lender understanding.

6. Consider Different Credit Facilities

Explore various lending solutions, term loans, revolvers, asset-based loans, and more. Qualification can depend on cash flow, collateral, enterprise value, and growth trajectory. Non-bank lenders may offer distinct advantages, such as less stringent regulations or more flexible terms. Discover more about working capital loan solutions and identify the best credit facility for your situation.

Modern financing extends beyond traditional options, mezzanine and venture debt, for example, can support growth without significant equity dilution. Match your loan structure to your business needs and long-term objectives.

7. Outline Best/Worst Case Scenarios

Perform sensitivity analysis around interest rates, lender-imposed structure, and total loan size. Pay special attention to non-negotiable covenants; identifying your ‘deal breakers’ early allows you to evaluate lender proposals effectively. Scenario planning ensures you are prepared for both upside and downside market shifts.

8. Review Existing Credit Agreements

Assess any active credit agreements to ensure your proposed refinancing does not breach covenants or require waivers. Tools like Cerebro’s Loan Compliance Navigator can help you navigate compliance and covenant complexities. Should you encounter an issue, Cerebro’s Loan Default Survival Guide provides action steps if a covenant is tripped during the refinancing process.

9. Select Counsel

Engage legal counsel experienced in loan financings similar to your planned transaction. Specialized experience is crucial to avoiding costly mistakes and expediting negotiations. If your current advisors lack this expertise, consider working with a seasoned transaction attorney or engaging capital markets professionals to guide your process. Learn more about how partnering with a capital markets team can benefit your financing journey.

10. Determine Your Timeline

Define key deadlines for acquisitions, growth plans, or refinance targets. Keep in mind that while some loans may close in 3–4 weeks, most require closer to 90 days, depending on transaction complexity. Notably, Reuters recently reported that U.S. banks saw steady demand for commercial loans for the first time in two years, indicating a stable climate for business borrowers. Using an intermediary like Cerebro Capital can help accelerate closing and deliver lender options efficiently.

Cerebro Capital’s commercial loan platform is transforming the way mid-sized businesses source and manage debt capital. By combining advanced data-driven technology with financial expertise, our platform streamlines the process of connecting companies with lenders and managing their loan portfolios. Access exclusive commercial lending resources and white papers for in-depth industry insights as you prepare for your next financing.

Frequently Asked Questions

What are the most important steps in refinancing a commercial loan?

Before refinancing, ensure your financial model is robust, your historical financials are complete, and your current credit agreements are thoroughly reviewed. Analyze your debt capacity using specialized tools like Cerebro Capital’s Debt Capacity Calculator, and consider seeking professional counsel experienced in loan transactions for optimal results.

How do I calculate how much debt my business can handle?

You can use tools such as Cerebro’s free Debt Capacity Calculator to assess your borrowing threshold based on your company’s financial health and market benchmarks. Lenders often look at metrics such as the debt service coverage ratio (DSCR) and leverage ratio when determining your eligibility.

What types of credit facilities should I consider when refinancing?

Depending on your business objectives and financial profile, consider various options such as traditional term loans, lines of credit, asset-based lending, and working capital loans. Each facility offers different benefits: for example, asset-based lending leverages your existing assets, while lines of credit provide flexibility for day-to-day cash flow needs. Explore more working capital loan options as you evaluate your choices.

How can I avoid violating loan covenants during refinancing?

Thoroughly review your current credit agreements for any restrictive covenants before pursuing new financing. Cerebro’s Loan Compliance Navigator can help manage this process and ensure your arrangements remain compliant.

What financial metrics do lenders prioritize when reviewing my business loan application?

Lenders generally prioritize cash flow, revenue trends, profitability, the debt service coverage ratio, and the leverage ratio. A strong, well-documented financial profile can lead to more favorable loan terms. Keeping detailed and accurate financial records is essential.

How do interest rates and economic trends affect my refinancing decision?

Interest rates directly impact borrowing costs; rising rates increase monthly payments and the total cost of borrowing. Lenders may also adjust their requirements in response to changing economic conditions. It is important to factor in both current rates and potential rate changes as you plan your refinancing.

What are the benefits of working with a capital markets team during a refinancing?

Engaging expert advisors helps you navigate complex transactions, compare lender offers, and remain compliant with all legal and financial requirements. Learn more about working with a capital markets team to streamline your approach and optimize financing outcomes with Cerebro Capital’s support.

What are common mistakes businesses make when refinancing a commercial loan?

Many businesses fail to prepare complete documentation, underestimate the time required to close, or overlook existing loan covenants. Leveraging Cerebro Capital’s platform, resources, and expertise helps ensure you are fully prepared for every step of the process.

Cerebro Capital’s commercial loan software is revolutionizing and modernizing the corporate loan process with data-driven technology. A team of financial and software experts combined their shared knowledge to build an all-in-one platform that creates efficient loan sourcing and portfolio management processes for middle market companies, PE firms, and intermediaries. Learn more about what makes Cerebro different.

Author: Matthew Bjonerud, Founder & CEO, Cerebro Capital

Updated: October 16, 2025

Cerebro Capital is committed to helping businesses secure the right financing through data-driven insights, objective guidance, and the broadest lender access in the market. Discover additional financing solutions such as working capital loans and strategies for managing debt by visiting our resource center.

Ready to get started?

Join the thousands of mid-sized companies who have used Cerebro.

Featured in

- info@cerebrocapital.com

-

12 W Madison St.

Baltimore, MD 21201 - Cerebro Capital

- @cerebrocapital