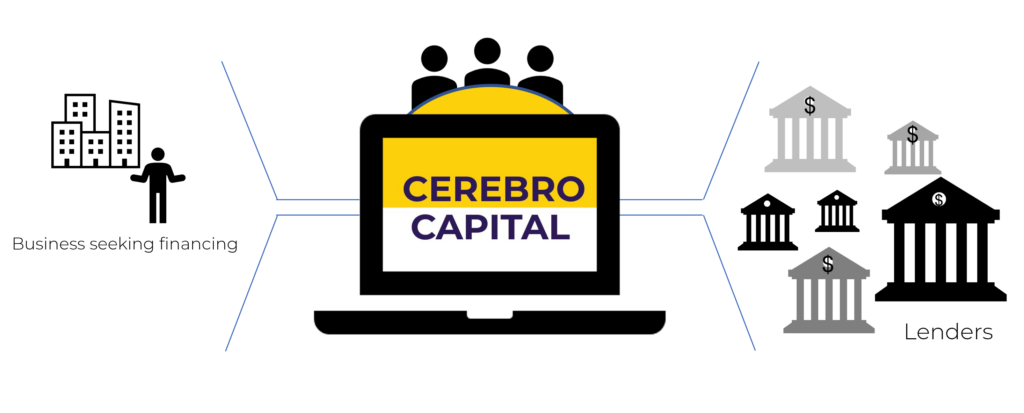

Discover all your business financing options- quickly and easily all in one place. With help from our Capital Markets experts and our data-driven marketplace of over 2,200 banks & lenders, you gain direct access to options that match your unique business story.

The Right Loan for Your Business

Find the right financing options available for your business from our powerful network of banks and lenders. Cerebro provides you tech-enabled lender matching based on your unique situation and our experts are here to help you.