BLOG

7 Ways to Get Debt Financing for Your Business: Comparing Your Options

Matthew Bjonerud

Founder & CEO

Does your business have ongoing efforts to raise capital? If so, it’s essential to be well-informed about the paths you can take to explore debt capital options for your mid-sized business. Each option has distinct characteristics and it is crucial to assess your options before committing to a specific path.

Understanding options for debt capital equips you to make informed decisions that align with your business objectives and long-term strategy. Below, we review each approach, highlighting their relative strengths and weaknesses for mid-market businesses.

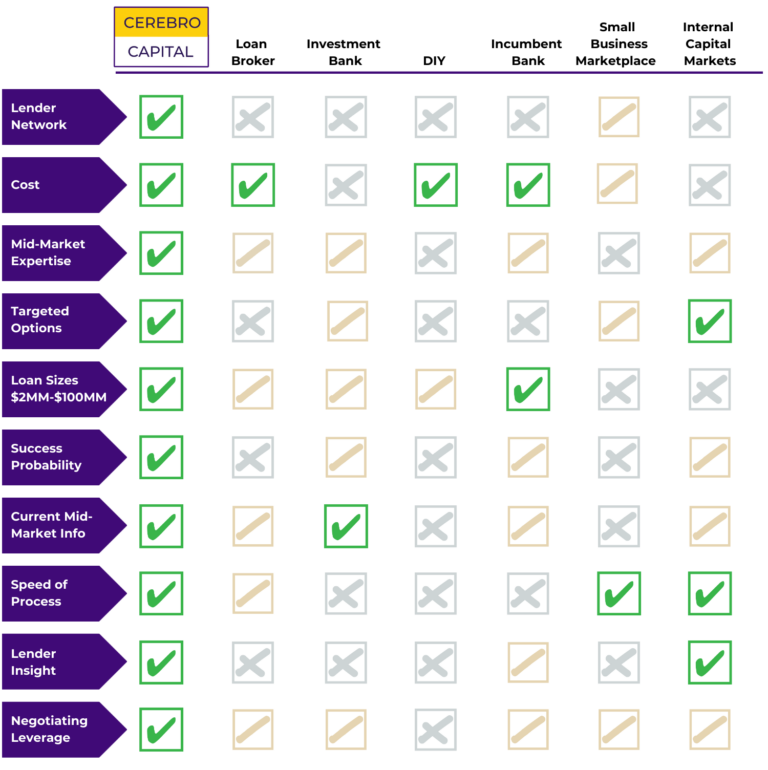

Loan Brokers

Loan brokers facilitate connections between borrowers and lending institutions within their pre-established network, acting as intermediaries to help businesses avoid the need to contact each lender individually.

Pros:

- Convenience: Brokers save your team time by leveraging their lender relationships, accelerating initial outreach and reducing the administrative burden on your business.

- Cost-Effective: Compared to building an internal Capital Markets function, using a loan broker is relatively affordable.

Cons:

- Limited Lender Network: Most brokers rely on a restricted group of “go-to” lenders, typically no more than five, leading to truncated loan options.

- Reduced Negotiation Leverage: Fewer lender options mean diminished power to negotiate favorable terms.

- One Person vs. Expert Team: Dependence on an individual broker can cause delays and reduce responsiveness compared to an institutional capital markets group.

- Limited Mid-Market Data: Loan brokers typically lack comprehensive mid-market insights since their perspective is limited to their small network.

- Missed Opportunities: Exposing your loan request to only a handful of lenders may prevent access to the full range of financing types or customized solutions for unique growth objectives.

Investment Bank

Investment banks provide specialized services for mid-market businesses, including underwriting, mergers and acquisitions (M&A), asset management, and strategic financial consulting. As outlined in the American Bar Association’s 2024 market trends report, the volume and sophistication of syndicated and direct lending are both climbing, another sign of evolving capital markets for growing firms.Pros:

- Financial Expertise: Investment banks deliver strategic lending advice, backed by extensive experience across multiple financing and advisory disciplines.

- Comprehensive Service Offering: Clients can access a suite of financial services beyond direct debt placement, ensuring thorough evaluation of capital needs.

Cons:

- High Costs: Expect substantial fees such as monthly retainers plus success or banker fees.

- Constrained Lender Reach: Their lender coverage is often narrower than lending platforms, limiting options for tailored solutions.

- Upper Mid-Market Primary Focus: Investment banks typically focus on transactions of $50 million and above, which may exclude many mid-market borrowers.

- Limited Options & Feedback: Periodic and restricted lender feedback means diminished negotiation leverage and a slower deal process.

DIY (Do-It-Yourself)

Handling your business’s search for financing independently can offer autonomy but also requires time, resources, and a solid knowledge of the lending landscape.Pros:

- Low Financial Cost: Not paying external advisors saves money upfront.

- Unrestricted Option Exploration: You dictate the search and aren’t bound by another party’s lender network.

Cons:

- Resource-Intensive: Direct outreach to each lender is laborious and can quickly consume significant management bandwidth, especially if the need for capital is time-sensitive.

- Limited Expertise: Without deep capital markets experience, it’s challenging to assess and negotiate optimal terms or navigate lender requirements.

- No Built-In Lender Network: Absence of a vast network curtails feedback, options, and leverage.

- Uncertain Funding Success: Your ability to close a financing deal is tied to your own expertise, industry connections, and available time.

Incumbent Bank

Longstanding banking institutions are a traditional source of business loans. Many borrowers seek out incumbent banks because of their reliability and established presence in the commercial mid-market.Pros:

- Competitive Costs: Incumbent banks often offer business loans at relatively low cost compared to specialty financing avenues.

- Direct Lending: Transactions are handled directly with the lender, not through intermediaries.

- Mid-Market Loan Sizes: Loan offerings typically align well with mid-market financing needs, usually from $2 million to $100 million.

Cons:

- Limited Product Suite: With only their own products to offer, borrowers won’t gain access to a wide lender marketplace.

- Variable Mid-Market Expertise: Insight into current mid-market conditions varies by institution.

- Restrictive Criteria: Underwriting standards can be restrictive and the rationale behind approvals opaque.

- Slower Process: Traditional banks may require longer timelines due to a lack of dedicated capital markets staff.

- Minimal Negotiating Power: The insight offered covers only that bank’s products, limiting leverage in negotiations.

Small Business Lender Marketplace

Technology-forward lender marketplaces connect borrowers with multiple lenders in a seamless digital environment, enhancing accessibility and loan comparison for small business segments.Pros:

- Robust Lender Network: Borrowers can review a variety of loan options from connected lenders.

- Expert Guidance: Small business-focused teams can help navigate the process.

- Technology Advantages: Real-time market data and digital platforms make comparison fast and efficient.

Cons:

- Loan Size Limitations: Most platforms prioritize loans under $2 million, leaving mid-market firms underserved.

- Narrow Market Scope: Insights are focused on the small business sector.

- Limited Mid-Market Leverage: While negotiating leverage exists, it typically applies to smaller deals, reducing efficacy for larger requests.

Internal Capital Markets

Building an internal Capital Markets team enables tailored financing strategies, analysis of current market trends, and execution of capital transactions.Pros:

- Deep Expertise: Dedicated professionals analyze and negotiate loan options specific to the business’s objectives.

- Delegated Engagement: The core management team benefits from a high-touch, hands-off process.

- Tailored Insights: In-house experts support optimal financing structures and lender negotiations.

- Streamlined Execution: Internal teams can accelerate the funding process through hands-on management.

Cons:

- High Overhead: Recruiting and retaining top talent is expensive.

- Network Constraints: Team size and contacts are inevitably more limited than external platforms operating at scale.

- Resource Allocation: Most appropriate for upper mid-market or larger, with minimums often exceeding $100 million.

- Restricted Reach: Smaller team sizes result in fewer simultaneous lender dialogues and potentially fewer customized loan options.

Why Cerebro Capital Is Different

Cerebro Capital was created for mid-size businesses seeking a smarter, more strategic path to debt financing. Leveraging proprietary technology and a true Capital Markets team, Cerebro streamlines, accelerates, and optimizes the funding process.

- Tech-Enabled Marketplace: Our data-driven platform connects mid-market borrowers to over 2,200 top-tier banks and non-bank institutions, offering unrivaled financing options. Learn more about our loan assessment capabilities.

- Patented Lender Matching: Save time and improve outcomes through intelligent, automated lender pairing, informed by $5.6 billion in recent committed loan proposals and real-time market intelligence.

- Expert Capital Markets Team: Our team brings more than 100 years of combined experience to guide you from initial evaluation to loan closing. For detailed information on our process and success stories, visit Cerebro’s engagement services and our client testimonials.

- End-to-End Comparison Platform: Compare multiple offers, term sheets, and lender feedback in one place. Cerebro provides transparency not just in costs and structures but in the unique features of each proposed loan.

- Non-Exclusive Solution: Continue negotiating with existing lenders or new entrants without exclusivity, which remains important as the global debt financing market is expected to reach USD 73.3 billion by 2033, according to Market.us.

- Fast and Efficient: Start your application in under 15 minutes; document upload launches matching in 24-48 hours. On average, term sheets arrive in 1–3 weeks, with typical funding completed in 60–90 days.

- Long-Term Partnership: Whether you need to refinance, acquire, or expand, Cerebro Capital supports multi-loan relationships for sustained growth and value.

Explore additional resources for specialized financing needs:

- Mezzanine Financing: For non-dilutive, flexible capital structures.

- Accounts Receivable Financing: Unlock working capital with receivable-backed solutions.

- Working Capital Loans: To support day-to-day operations.

Cerebro’s blend of technology, expert advisory, and marketplace scale is designed specifically for mid-market businesses seeking strategic funding. See how Cerebro Capital can improve your next deal, or contact us for a confidential assessment.

Frequently Asked Questions

What financing options are available for mid-market businesses?

Mid-market companies can access a broad spectrum of debt solutions including term loans, revolving lines of credit, asset-based loans, mezzanine debt, and accounts receivable financing. Each of these fits different stages and business needs. Cerebro Capital’s marketplace is optimized to help you navigate and compare these choices efficiently. Learn more about mezzanine financing options and receivable financing specific to mid-market borrowers.

How do I choose the best loan option for my business?

Assess key criteria such as required capital, repayment flexibility, interest rates, collateral needs, and term length. Comparing offers side-by-side ensures you find the best match for your cash flow goals and risk appetite. Cerebro Capital’s loan assessment tool and data-driven platform are designed to help mid-market companies evaluate options quickly.

What metrics do lenders focus on when reviewing my application?

Lenders will scrutinize your company’s cash flow, profitability, debt-to-income ratio, leverage, and business credit score. Having strong, verifiable financial statements, consistent revenue, and a clear repayment plan will increase your chances. Demonstrated stability and healthy coverage ratios are especially important for mid-market financing through Cerebro’s network.

How does asset-based financing work, and is it right for my company?

Asset-based financing uses your business assets, such as accounts receivable or inventory, as collateral to secure funding. This approach is ideal when you need working capital and have substantial business assets. Learn more about the process and benefits by visiting Cerebro Capital’s guide to accounts receivable and working capital loans.

What is the typical timeline for securing funding through Cerebro Capital?

Cerebro processes loan requests rapidly, most clients complete initial applications and document uploads in less than an hour, receive term sheets in 1–3 weeks, and secure funding within 60–90 days, leveraging our proprietary matching and lender network.

What are the risks of overleveraging, and how can my business avoid them?

Overleveraging can lead to liquidity issues, difficulty servicing debt, and limited strategic flexibility. Cerebro Capital recommends actively monitoring debt ratios, ensuring healthy cash flows, and comparing loan terms to maintain a balanced and sustainable capital structure over time. As Globewire News notes, businesses are seeking advanced financing strategies to stay resilient in fluctuating economic conditions.

How do I compare multiple lender offers effectively?

Use an organized, side-by-side approach, focus on not just the interest rate but repayment flexibility, covenants, fees, and lender reputation. Cerebro Capital provides a platform to automate term sheet comparisons and offers advisory support to interpret subtle differences that impact your long-term business goals.

Still have questions about debt financing? Contact Cerebro Capital for personalized guidance or request a loan assessment to discuss your current needs and options.

Author: Matthew Bjonerud, Founder & CEO, Cerebro Capital

Updated: October 16, 2025

Cerebro Capital is committed to helping businesses secure the right financing through data-driven insights, objective guidance, and the broadest lender access in the market. Discover additional financing solutions such as working capital loans and strategies for managing debt by visiting our resource center.

Related Content

The world of middle-market lending has changed. Before COVID-19, traditional lenders showed flexibility as they worked to expand their books of business.

Increase the Chances of Closing a Loan

Significant disruptions to the lending landscape in the past four months have left corporate borrowers scrambling to stay on top of changing requirements

CFOs need to be constantly aware of how their company’s financial performance and market shifts affect its debt capacity, which is the best measure of your business’ ability to borrow.

Ready to get started?

Join the thousands of mid-sized companies who have used Cerebro.

- info@cerebrocapital.com

-

12 W Madison St.

Baltimore, MD 21201 - Cerebro Capital

- @cerebrocapital